Orca Global: July 2022 Investment Newsletter

Disclaimer: This page, including any links or posts, is not an offer or invitation to subscribe for shares in the fund. Please read the full disclaimer at the end of this page.

This was originally sent to investors of Orca Global Management on 15 August 2022.

What happened in July?

July was a tough month for us as we got caught short in unexpected rallies. Our lower PnL was driven by two catalysts.

1. Convex Finance

The first was with $CVX, the reward and governance token for Ethereum based DeFi protocol Convex Finance. If you are unfamiliar with Convex, it is a complicated protocol to explain as it exists purely as an application layer for another DeFi protocol Curve Finance, but here is the gist of it:

By Total Value Locked (TVL: the $ amount users have “locked” in to DeFi protocols), Convex ranks 6th among all protocols with more than $4 billion worth of assets deposited on the platform.

Convex was created to allow users to maximise the yields on Curve more efficiently.

What is Curve? Curve is one of the largest DEXs (Decentralised Exchange) that revolutionised the DeFi game by employing their own mathematical swapping formula (“StableSwap Invariant” versus the traditional “Constant Product Formula”) that allows users to swap large amounts of tokens with much less slippage than in traditional DEX models. Curve offers its own token $CRV as a reward (i.e. the “yield”) to LPs (Liquidity Providers: the users who provide liquidity into DEX “pools”. Other users trade against these pools by swapping their tokens for another in the pool), but since giving away your own token will create a constant stream of selling pressure, Curve created a way to incentivise users to lock up their $CRV tokens, to receive a higher reward yield. The longer you lock up your $CRV tokens with Curve (ranging from 1~4 years), the higher yield you are entitled to receive. To further increase incentive to hold, Curve designed their protocol in such a way that the more $CRV you lock up, the more voting power you must vote for which pools Curve allocates additional yield to.

What Convex does is it aggregates a tonne of $CRV tokens, so that users, instead of locking up their own $CRV tokens for 4 years to get the maximum available yield, can give their $CRV to Convex for a much shorter duration (flexible) and receive the same yield as they would have gotten had they locked up their $CRV for 4 years. Whereas only a “whale” (a user/institution with a large balance sheet) with the willingness to lock up tokens for a long period could maximise the Curve yields, now even a small-time retail player could do so as well. So, this is why Convex is often referred to as a “Curve yield booster”: they provide liquidity to an illiquid investment whilst maintaining the extra yield that is the term premium, all while giving the user optionality without charge to shorten the duration of their Curve investment if they choose.

To some this is the genius of DeFi’s creativeness and genius tokenomics (token-economics); to others this just looks like a flawed game of layered incentives just waiting to collapse on itself. We see it as a fluid scale where the needle is closer to the former in a bull market and closer to the latter in a bear market.

What we didn’t anticipate was a sudden spike in $CVX - over 60% in a day- when the broader market sold-off (for example Ethereum, which Convex is built on, was down more than 8% the very same day). Despite trading light and cautiously due to the reasons we mentioned in our June newsletter (e.g. illiquidity spikes) this move caught us off-guard and drove our PnL lower early on as we were short the wrong token. We were able to recoup some of our losses as other tokens sold-off along with the rest of the market but faced losses again when the market reacted to the Ethereum merge update.

2. Ethereum Merge

This brings us to the second event that drove our negative performance: the Ethereum Merge. This is a fairly technical concept but since it is undoubtedly the most focused and highly anticipated event in crypto this year, we will attempt to explain what it is. If the statement “the Merge is Ethereum's transition from proof-of-work (PoW) to proof-of-stake (PoS)” doesn’t make sense, the below explanation may be of use to you:

This is an explanation we offered to our non-crypto friends a couple of weeks ago, using an analogy of a car:

The Beacon Chain is essentially Ethereum’s next update which co-exists in the test stages alongside the current form of Ethereum (referred to as “Mainnet”).

If Ethereum was a car, there have been long-running plans to upgrade its engine. The current engine (Mainnet) runs on diesel, and it has been decided that the community wants to swap out the outdated diesel engine for an electric one, whilst keeping the other components of the car the same.

Since this is a non-trivial task, engineers have built an electric engine (Beacon Chain) that they’re testing out on the side before they fully swap the engine. This electric engine can be run in another car body to test out its condition/quality concurrently to the current diesel engine as to not disrupt the everyday use of the original car.

While Ethereum Mainnet (the Ethereum we all use today) processes transactions and handles smart contract interactions, the Beacon Chain is purely a ledger of accounts that conducts and coordinates the network of stakers: the diesel engine is being used in an actual car to take us from A to B, while the electric engine is only being trusted to see if it can simply output power.

In a little more technical terms, this means that the Beacon Chain is still just a “consensus layer” and it has existed as a separate chain from Mainnet (or the "execution layer") since its genesis. The plan is to swap out the current Proof-of-Work (PoW) algorithm on the execution layer today and replace it with the proof-of-stake (PoS) consensus protocol that the Beacon Chain has been working on. This is the process of the “merge”: combining the new consensus layer with the existing execution layer and stopping the use of mining.

The idea is that the Merge will have an immediate and profound impact on the carbon footprint of the Ethereum network whilst also setting the stage for future scalability upgrades such as sharding. In PoS, the Blockchain’s consensus comes from users (stakers) who lock up their token (in this case $ETH); in PoW, the consensus comes from people (miners) who secure the network with computing power (by solving increasingly difficult mathematical problems, which use a lot of power).

In the car analogy, the Merge is the act of the engine-swapping.

The analogy is useful in explaining further concepts such as staking, as well as relevant major protocols like Lido Finance. If you have any questions, please feel free to reach out to us, as this is THE concept to understand in crypto this year.

And this is what caused the rally that led to our second round of losses. On the 14th of July at 14:00 UTC, Ethereum engineers had a meeting (live streamed on YouTube) where Tim Beiko, an employee with the Ethereum Foundation who is in charge of running the core protocol meetings, proposed the week of September 19th as the new tentative target date for the Merge which faced no objections from other members in the meeting. Ethereum immediately rallied ~14% and was up more than 30% within 3 days, taking the rest of the market with it. What confused us was the fact that it had been widely known and expected for months that September was when the merge was taking place (was very commonplace knowledge); we did not expect the initial rally to continue. As Figure 1 shows, the proposal for the merge date marked the bottom for the macro markets too, as the S&P 500 found its bottom for July, literally to the hour of the comment:

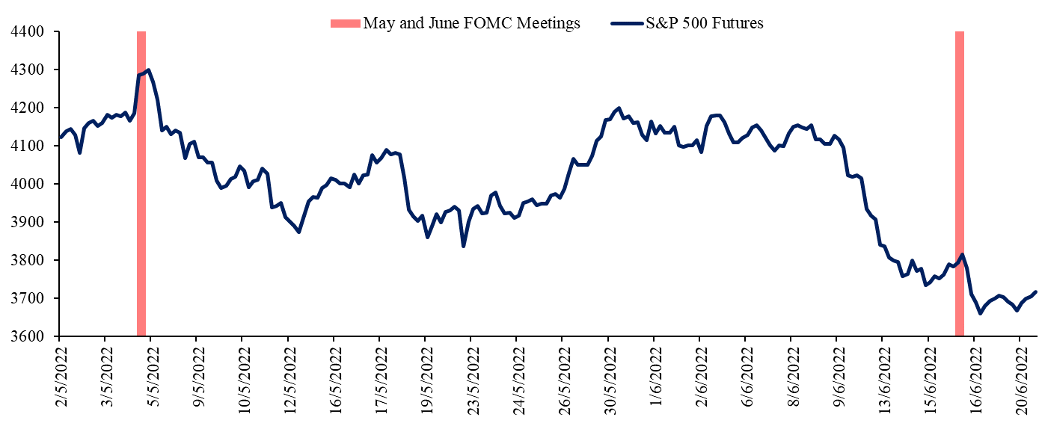

The macro catalyst that marked the local bottom in equities was the July FOMC, and as we explain in further detail below, this to us didn’t warrant the buying that happened on the day. It looked more like the May and June FOMCs when the market rallied on the statement/presser, then quickly reversed in more violent fashion the next day (Figure 2). So, with this backdrop, and the rally in crypto being from the simple fact that Ethereum developers didn’t object to the suggestion of what everyone already knew, the pump looked like a very attractive “fade the rally”. And we were very wrong.

More on July and our views

Towards the end of July, we were still of the consensus view that we were in a bear market rally in US risk assets. For many, particularly for Fed watchers and rates traders, the equity rally didn’t quite make sense. Bond markets globally were doing a thing of their own as Bloomberg’s aggregate US long treasury index was up 2.67% in July, 30yr TIPS up 8.55%, Italian bond yields down 63bps in 6-trading days, and bund yields down 1.9% to 0.8% in a month (a roundtrip from 0.8 to 1.9 to 0.8 in fact). In equities, the last week of July was the best week in 2 years. S&P 500 rallied 9.22% in July and growth outperformed value. The JP Morgan equity desk attributed the moves to simple portfolio re-allocation (institutions, large asset managers, etc) while the Goldman Sachs equity desk attributed this to CTA flow: two classic reasons you give when you don’t actually know what just happened (it especially seemed like weak arguments since the timing of portfolio re-allocations or flows didn’t make sense). So, was risk appetite REALLY back? We didn’t think so since over the month of July the MSCI EM index was slightly down, and MSCI All-Country world index excluding US was only up 3.42%. So, it seems it was more a US centric rally than a broader risk on sentiment. If markets are a short-term voting machine, it was hard to grasp what it was everyone was voting for. The rates markets seemed to be positioning for a world in which the Fed brings down interest rates soon, while inflation also comes swiftly under control, all without damaging corporate returns enough to dent the stock market. This was quite the rosy scenario market participants were voting for.

Overall, price action seemed to have been implying a Fed that quickly reverses course, whilst simultaneously implying a declining economy and falling inflation, while corporate earnings sail on unscathed: confidence in the Fed was suddenly so high. High confidence in the Fed in a year of Fed insider trading scandals, Powell’s insistence that inflation was transitory (despite every soul in markets saying that it wasn’t) and his quick reversal once he got renominated as Fed chair…? Very non-ordinary times.

Just look at the July FOMC statement + Powell’s testimony, the catalysts for last month’s rally:

The FOMC decided to remove forward guidance in favour of being data dependant (much like the ECB did the week before),

They also left a high bar for policy alteration (the “pivot”): “Over coming months, we will be looking for compelling evidence that inflation is moving down, consistent with inflation returning to 2%”,

and explicitly mentioned being open to another 75bps: “While another unusually large increase could be appropriate at our next meeting, that is a decision that will depend on the data we get between now and then”

To some this may not be outright bearish, but this didn’t scream “BUY EQUITIES!” to us.

Some other points that made us think we were just in a bear market relief rally:

Earnings hadn’t really been bullish:

Beats have been average at best. Deutsche Bank’s Chadha summarised the recent earnings season as, “in line for the median company but below average in the aggregate”

More from Chadha on the earnings growth under the surface: “On a sequential basis quarter-on-quarter, underlying earnings adjusted for seasonality [the second quarter tends to be strong] are on track to fall sharply by -4.5% quarter-on-quarter, one of the steepest declines over the last decade, comparable to those seen in the early stages of the pandemic”

Equities usually hit bottom once forward earnings estimates have been cut to a low, but not this time. From a Bank of America research note: “During the last five recessions, the S&P 500 bottomed after estimates were revised down, except in 1990 when forward EPS remained flat. But estimate cuts are just starting now and even with those modest cuts, forward EPS is still up 7% since the market peak.”

So, if the bottom was already in for equities, then that would imply that an earnings recession will be avoided altogether.

Fed will continue to track lagging indicators like CPI and US employment and policy will remain tight until first quarter next year. QT has just started and will double in September.

Fed tightening is starting in a world where global economies are facing a significant global slowdown, for example Europe but more importantly China, an exporter and producer of goods.

Valuations are still high in US equities - the bottom in equities aren’t usually marked with high/expensive valuations

VIX hasn’t gone ballistic yet, but this is a weaker argument since we believe the source of the bear market has been rather different to ones that induce VIX spikes (no earth-shattering surprise catalyst like covid or a major bank going under).

Seasonality: August to October in mid-term years is seasonally weak.

But as is clear now, we were wrong in assuming these factors would bring the market lower. There is time and potential for these things to take effect with a delay, and of course it is possible that the Fed will come back in September with a hawkish surprise which will coincide with when the merge happens and will create a buy-the-rumour-sell-the-fact scenario. In any case, what is important now is that CPI missed last week (8.5% YoY headline inflation vs 8.7% expected) and that risk assets have been very bid.

The balance among the variables that drive price action is not static in any asset class, and this is no different in crypto. After crypto markets peaked in November last year, and macro markets turned a month later, any regression or PCA (or just by experiencing the markets), it was clear that all eyes from all asset classes were on inflation, everything else was secondary. This current crypto winter has been no exception, with only the Luna meltdown and 3AC sell-offs being the crypto-inherent drivers.

To many this probably still holds true but seen from a different perspective, we would argue that inflation is less of a threat today than it was two years ago. Of course, investors still care about inflation but in aggregate they seemed to show their confidence in both tighter monetary policy and ability for that monetary policy to sufficiently damage the economy, enough to at least bring inflation lower in the medium term. Perhaps this responds directly to what we said earlier: “Price action seemed to be implying a Fed that quickly reverses course, whilst simultaneously implying a declining economy and falling inflation, while corporate earnings sail on unscathed: confidence in the Fed was suddenly so high”. It is possible that it is in higher rates that the market is showing confidence in, not specifically the Fed. University of Michigan surveys (the most widely watched survey data in the US) show that despite the surge in fuel and housing prices (and general inflation), American incomes are meeting consumer needs, and that Americans expect gasoline prices to decline over the next five years. One reason mentioned by Bloomberg journalist Matthew Winkler on why multi-decade high fuel prices may not have proven as painful as their ubiquitous reporting suggests is that current fuel expenditures amount to 3.5% of total consumer spending versus an average of 3.6% in monthly data going back three decades. While fuel at $5/gallon in June was $1 more than in the previous high back in 2008, gas expenditures accounted for 4.5% of spending back then, which means the price of fuel would need to rise an additional 35% to about $6.60/gallon to have the same impact on consumers today. It is also important to remember that real disposable income is still greater today than at any point prior to 2020.

Furthermore, despite inflation being the absolute worst thing in the world (all over the radio in at least Singapore, New York, and London: it’s probably one of the few things in society that people of all backgrounds can feel and complain about which is why it makes it such an incredible political topic) the market is not particularly bidding up assets that offer protection from inflation. During the first quarter this year, net inflows into inflation-protected ETFs declined more than $12 billion to $718 million. And during the second quarter, there was a net outflow from these ETFs.

If inflation is why the market was bearish (including us), but American consumers are not ACTUALLY feeling it + investors are not demanding protection from it, perhaps this negates the bearish factor considerably.

How we are trading this:

Although still cautious of downside moves, we have been trading long. We have revamped our portfolio construction and have incorporated a few new strategies that we had been working on for a while. This is what our current portfolio looks like:

Long basket: We are currently building out long positions in various alt-coins that we believe will outperform the majors ($BTC and $ETH) in a bull market.

Leveraged topside derivatives: positions that give us inherent leverage to the upside (NOT taking any outright leverage).

RV basket: An equal weighted basket of long futures versus short futures. 10~20 coins for each side and rebalanced weekly. This is a market neutral strategy that, over time, is structured to return positively regardless of overall market direction and lowers the variance and volatility of our entire portfolio.

Systematic hedging: This section of the portfolio algorithmically takes into consideration our delta exposure in the directional portions of our portfolio and executes optimal hedges (via options) given various defined parameters that are both systematic (higher frequency) and discretionary (lower frequency).

Early-stage deals: We have been active in sourcing deals and have reviewed quite a few early-stage investments. As we mentioned in last month’s newsletter, the space is unfortunately quite saturated with low quality projects, but we have been in talks with a few exciting protocols and have put pen to paper for one such protocol (which we will announce once the deal is public).

We are confident in this portfolio and confident in making back what we have lost this year.

Interesting crypto events in July

European Economic and Monetary Affairs Committee negotiators struck a provisional political agreement with the Council on new rules on crypto-assets (MiCA)

Crema Finance (concentrated liquidity protocol on Solana) was hacked. OtterSec (blockchain audit firm) mentioned that Crema was hacked for over $6 million

Vauld (Singapore-based crypto trading and lending platform with operations in India) halted client withdrawals and hires advisors for potential restructuring

Aave (dApp on Ethereum that facilitates lending and borrowing, with a TVL of $12 billion) announced GHO, a native decentralized, collateral-backed stablecoin pegged to USD

Uniswap liquidity provider hacked for $8 million in phishing attack. Smart contract security firm PeckShield told The Block that the liquidity provider had fallen victim to a phishing tactic, which allowed the hacker to steal more than 7,500 ether ($8 million)

Unofficial Ethereum Merge date was being circulated online for 19th September (subject to change)

Harmony’s (L1) core team has proposed a hard fork to mint billions of new harmony (ONE) tokens. The proposal is part of the plan to reimburse victims of its bridge hack last month. In June, a hacker stole $100 million worth of crypto assets locked on the Harmony-run Horizon bridge on Ethereum. Since then, victims have asked for a refund

Further Disclaimer:

The following important information relates to the use of Orca Global Management’s substack publications. Orca Global Management is a fund registered in the Cayman Islands. This publication is directed only at persons who: a) Are expert investors who fall within the definition of Accredited Investor b) Are otherwise permitted to read this publication in compliance with the governing laws of their respective jurisdiction. It is not directed at or intended for retail clients nor general public dissemination. Any person considering an investment into Orca Global Management’s fund must ensure that they are suitably qualified, experienced and knowledgeable on such investments considering jurisdictional rules, regulations and restrictions, tax implications, residence or domicile and their financial circumstances. Past performance is not a guide to what may happen in the future. Prospective investors should be aware that the value of their investments could fall as well as rise. Any investment carries the risk of potential total loss of capital and investors may not get back the value of their original investment. Information on this publication may include data and opinions derived from third party sources. Orca Global Management does not accept liability for the accuracy or completeness of any such information or opinions which can be subject to change without notice. Furthermore, the information provided does not constitute an offer to buy or to sell cryptocurrencies or any other financial instrument, nor does it constitute investment, legal or tax advice. Details relating to the investment including the risk disclosures can be found in the Private Placement Memorandum. This brief statement cannot disclose all the risks and other significant aspects of the various markets traded by Orca Global Management.